New—Payout Plus Benefit Option

Not available in New York

Payout Plus is a benefit option with a Pacific Life structured settlements annuity that provides the potential for payments to increase after the first year. Payments are tax-free1 and linked to S&P 500® index performance, subject to a cap. An adjustment rate that is applied may cause a payment to decrease, but never below the guaranteed minimum paid out in the first year, called the baseline payment.

Consider This for Clients Who:

How Payout Plus Works

After the first year, payment changes are determined annually as follows:

-

The S&P 500 index return is measured annually and serves as the starting point for the payment calculation.2

-

The S&P 500 index return is subject to a cap rate and a participation rate.

- A participation rate is how much of the positive index return is used in calculations. The minimum participation rate is 100%.

- A cap rate is the maximum percentage of index return used and limits the potential positive index return that may be applied.

- If the index return is 0% or negative, the participation rate and cap rate do not apply. A negative index return is always adjusted to 0% but payment amounts can decrease due to an adjustment rate, which is discussed more below. The result of these modifications is called the “adjusted index performance.”

-

The adjustment rate is subtracted from the adjusted index performance. The higher the adjustment rate, the higher the cap rate, which may help capture more of a positive index return for payment increases. However, a higher adjustment rate causes a larger reduction when applied to the adjusted index performance and may result in a payment decrease.

- A maximum adjustment rate is set by Pacific Life and will not change after issue. For example, if the maximum rate is 5%, an adjustment rate between 0% and 5% may be applied.

- The adjustment rate will never cause a payment to be below the guaranteed baseline payment, as the baseline payment is always protected.

- If the adjusted index performance is higher than the adjustment rate, the payment will increase. If the adjusted index performance and the adjustment rate are equal, the payment stays the same. If the adjusted index performance is lower than the adjustment rate, the payment will decrease.

How the Cap Rate Works

The cap rate is applied when the index return exceeds the cap rate percentage. Pacific Life compares the index return and the cap rate to determine the percentage of the index return used in calculations.

The hypothetical graph is for illustrative purposes only and assumes the 100% participation rate.

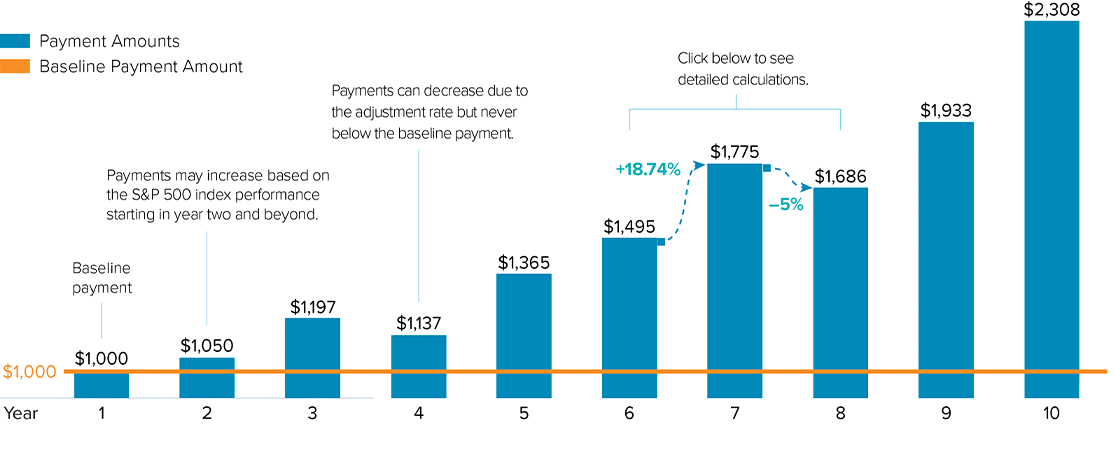

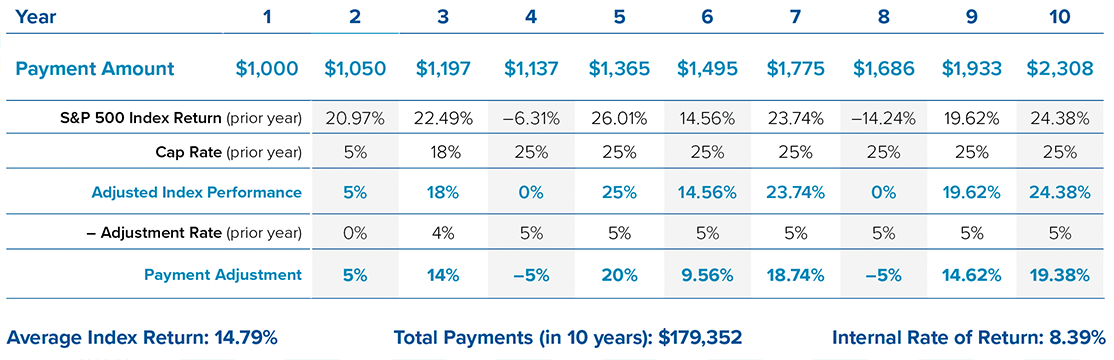

Payout Plus in Action: A Hypothetical Example

After a life-changing accident, Audrey is anticipating a personal injury settlement. At 50 years old, she wants to turn potential settlement funds into payments for 10 years until she plans to start drawing from her retirement fund. Audrey chooses a structured settlements annuity with the Payout Plus benefit option. She starts her payments in year 1, receiving the $1,000 baseline payment each month of that year. Let’s see how her payments might increase from there.

Hypothetical Results and Assumptions for Determining the Payment Amounts

Audrey's Potential Payment Increases

The hypothetical graph is for illustrative purposes only and uses historical annual S&P 500® index returns, without reinvestment of dividends, from April 15, 2016, to December 15, 2025. Assumes a female, age 50, 100% participation rate each year, an immediate 10-year period certain benefit, premium of $114,793, and a baseline payment amount of $1,000.

Historically, the S&P 500 Index Has Had More Positive Returns than Negative Returns

While past performance is not an indication of future results, the S&P 500 index was chosen to link to payment increase potential because it has delivered a significant number of positive returns over its history. The past 55 years of history is shown below. Depending on the current cap rate, the entire index return might be used in calculations.

S&P 500 Index (rolling returns January 1970 to December 2025)

Returns for each year start in January and end in the following year. For example, returns for December are December 15, 2024 to December 15, 2025. Negative index returns will not cause a payment amount to go down.3

When the measurement period starts depends on the funded date. All measurement periods start and end on the 15th of the month or most-recent prior business day.

For Use With Clients

For more information, contact your Structured Settlements Consultant.

Pacific Life Insurance Company

Pacific Life & Annuity Company

26-12A

SSQ4948-01 6/26 E229

1Excludable from gross income under Internal Revenue Code (IRC) Section 104(a)(1) or (2).

2The return is calculated over a measurement period, which begins on 15th of the month after the funded date. Subsequent periods will start on that date each year. If the 15th the month is not a business day, we use the prior business day's price. The S&P 500 index returns do not include the reinvestment of dividends.

3Source: Bloomberg, Inc., as of January 20, 2026

Contract Form Series: ICCII:10-1213, Rider Series: ICC25:20-1290. State variations to contract form series and rider series may apply.

The Payout Plus benefit option is not an investment or security and does not participate directly in the stock market or any index. It is an insurance product designed to help a client prepare for his/her future.

Selecting an optional index-linked benefit option will result in a lower guaranteed minimum payment amount than when selecting a traditional structured settlements annuity. The guaranteed payment also can vary based on the annuity type and period selected. Initial payments may or may not step up to a new guaranteed minimum value, depending on what benefit option(s) you choose.

The S&P 500® index is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and has been licensed for use by Pacific Life Insurance Company. S&P®, S&P 500®, SPX®, SPY®, US 500™, The 500™, iBoxx®, iTraxx®, and CDX® are trademarks of S&P Global, Inc., or its affiliates (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Pacific Life. Pacific Life’s product is not sponsored or, sold by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500® index.

Pacific Life reserves the right to change or modify any non-guaranteed or current elements. The right to modify these elements is not limited to a specific time or reason.